The Search For Income

Interest rates have risen steadily over the past six months but remain low by historical standards. That means the traditional high-quality bonds that many of us owned for decades are not doing the job for investors looking for income, while the potential for interest rates have risen steadily in recent months brings more risk in the bond market than has been evident historically. Here we look at some income ideas that may help with these challenges. When investors think about income, or yield, they would normally think bonds first. More on that below. Next they might think about getting extra yield from their stock portfolios, maybe with a dividend strategy that might be heavy on real estate investment trusts (REITs) and utilities. While we don’t have anything against using those types of strategies for a portion of a portfolio to get some yield, they can also carry unwanted interest rate sensitivity if rates rise. We highlight some equity income ideas that we would expect to perform well in a rising rate environment for you to consider when building your portfolio.

While the actual yield bank loans may offer in the future is not certain, this analysis does show that bank loans provide an attractive income option relative to other fixed income alternatives for investors looking to limit interest rate risk at the beginning of a possible rising rate cycle. It’s important to understand the trade-off between interest risk and credit risk. We know there is no such thing as a free lunch. That additional income compensation comes with assuming credit risk (the risk of a default or credit downgrade) and the risk that prices drop sharply in a risk-off environment if demand suddenly dries up.

While the actual yield bank loans may offer in the future is not certain, this analysis does show that bank loans provide an attractive income option relative to other fixed income alternatives for investors looking to limit interest rate risk at the beginning of a possible rising rate cycle. It’s important to understand the trade-off between interest risk and credit risk. We know there is no such thing as a free lunch. That additional income compensation comes with assuming credit risk (the risk of a default or credit downgrade) and the risk that prices drop sharply in a risk-off environment if demand suddenly dries up.

Income Idea #1: Energy

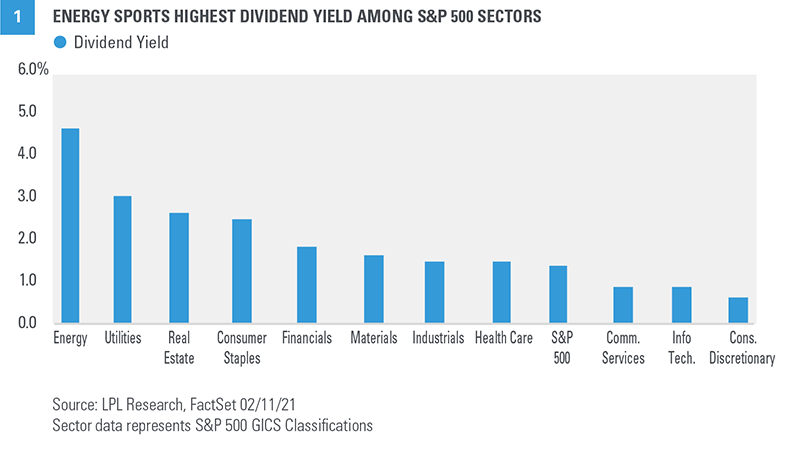

The first idea is energy stocks. You may be surprised to learn that the energy sector currently yields about 5% based on dividends paid in 2020, topping all S&P 500 sectors [FIGURE 1]. In this month’s Global Portfolio Strategy report, we upgraded our view of the energy sector to neutral. Our increased optimism was driven primarily by three factors. First, as we get closer to a fully reopened economy and travel activity picks up—potentially in the second half of this year—energy is likely to be a big beneficiary. Second, our technical analysis work revealed attractive upside potential based on recent price appreciation after an extended period of weakness. Third, we see the sector as attractively valued, especially when considering the income potential.

Income Idea #2: Banks

You may be surprised to see banks on here as another income idea. The financials sector, which we upgraded in our January Global Portfolio Strategy report, carries a dividend yield of 1.9%, but banks yield 2.6%, based on the S&P 500 Bank Index. Although plenty of bond strategies carry yields in that range or higher, banks do not bring the interest rate risk that bonds do. Historically, bank stocks have exhibited positive correlation to interest rates (the stocks have tended to outperform as yields have risen). Bank stocks also tend to like a steepening yield curve—long-term interest rates rise faster than short-term rates—which we expect to see over the balance of 2021 as the economic recovery gains steam. We also expect bank dividend payouts to rise over the next year or two as the Federal Reserve eases up on payout restrictions. More progress on vaccine distribution should also enable a fully re-opened economy and drive stronger economic growth, which should bode well for the profitability and, therefore, dividend payout potential for the financials sector. Yields from banks may not look great on the surface—certainly not compared to the energy sector or some of the higher yielding segments of the bond market. But in a low rate environment with rates more likely to rise than fall, in our view, we think banks can make sense for income oriented investors with an eye toward total return.Income Idea #3: Bank Loans

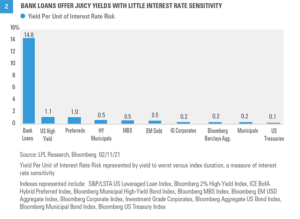

There are a number of fixed income options that may be suitable for income-oriented investors. For investors looking to limit interest rate risk, we believe bank loans, which we upgraded this month, may be an attractive option due to the improving economic environment and limited rate sensitivity (see our February Global Portfolio Strategy report for more details). [FIGURE 2] ranks the major fixed income sectors by income per unit of interest rate risk. Since fixed income indexes have different degrees of interest rate sensitivity, this exercise allows us to determine compensation for taking on interest rate risk. Bank loans are an obvious standout by this measure, offering potential yields in the 4% range with extremely low interest rate sensitivity. While the actual yield bank loans may offer in the future is not certain, this analysis does show that bank loans provide an attractive income option relative to other fixed income alternatives for investors looking to limit interest rate risk at the beginning of a possible rising rate cycle. It’s important to understand the trade-off between interest risk and credit risk. We know there is no such thing as a free lunch. That additional income compensation comes with assuming credit risk (the risk of a default or credit downgrade) and the risk that prices drop sharply in a risk-off environment if demand suddenly dries up.

While the actual yield bank loans may offer in the future is not certain, this analysis does show that bank loans provide an attractive income option relative to other fixed income alternatives for investors looking to limit interest rate risk at the beginning of a possible rising rate cycle. It’s important to understand the trade-off between interest risk and credit risk. We know there is no such thing as a free lunch. That additional income compensation comes with assuming credit risk (the risk of a default or credit downgrade) and the risk that prices drop sharply in a risk-off environment if demand suddenly dries up.